Today we’re going to talk about a subject that affects many future travellers… Bank fees abroad and how to avoid them! On our side we use a Swiss bank (postfinance) for the good and simple reason that we have no choice! 🙂

If you are also Swiss, we invite you to have a look at our article comparing the offers for Swiss travellers or at out page dedicated to Neon, the swiss mobile-bank.

N26 is a mobile bank that we’ve heard a lot about from other travelers from France (or elsewhere in Europe). So we thought a short article to introduce you to their concept would be in order. Originally, it was impossible for Swiss residents to have an N26 account, but things have changed over the last 2-3 years. N26 is now available in Switzerland, and we thought we’d take a closer look at their offer to see if it’s worth your while.

Bank N26 (ex: Number 26): who are they?

N26 was originally called Number 26 and was founded in Berlin. At the start it was not a bank as such in the sense that they depended on another bank for everything that was legal. Since summer 2016 this is no longer the case. N26 has obtained its banking license from the European Central Bank and is now a fully-fledged bank.

N26 has the particularity of being what is often called a neo-bank or mobile bank. Understand that absolutely everything related to banking is done online. There are no physical counters!

Account opening, identity verification, data entry, everything is done directly from your computer or smartphone.

N26 is also a start-up that is on a roll! Founded in 2015, it already has more than 8 million users across Europe.

Why should I use an online bank for my trip?

The main reason why travellers turn to mobile banks is simply the cost! Indeed, the tariff structure of traditional banks is often not thought out (or at least not well thought out) for travellers.

Withdrawal fees, aberrant exchange rates or restrictions on use abroad are often the reason why people choose a mobile bank to complement their traditional bank when they travel.

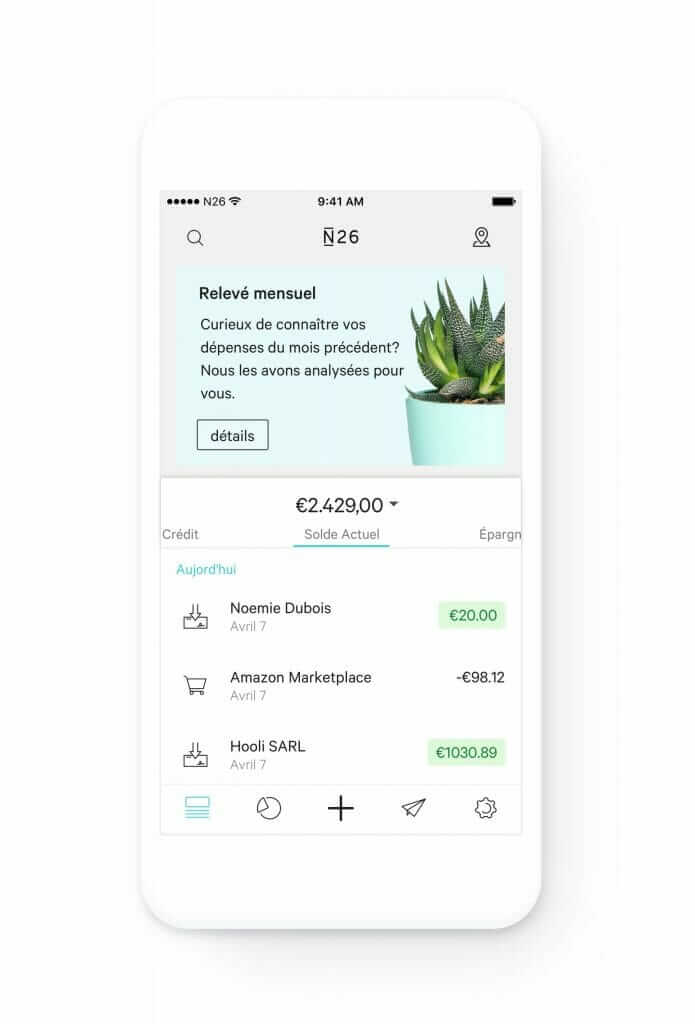

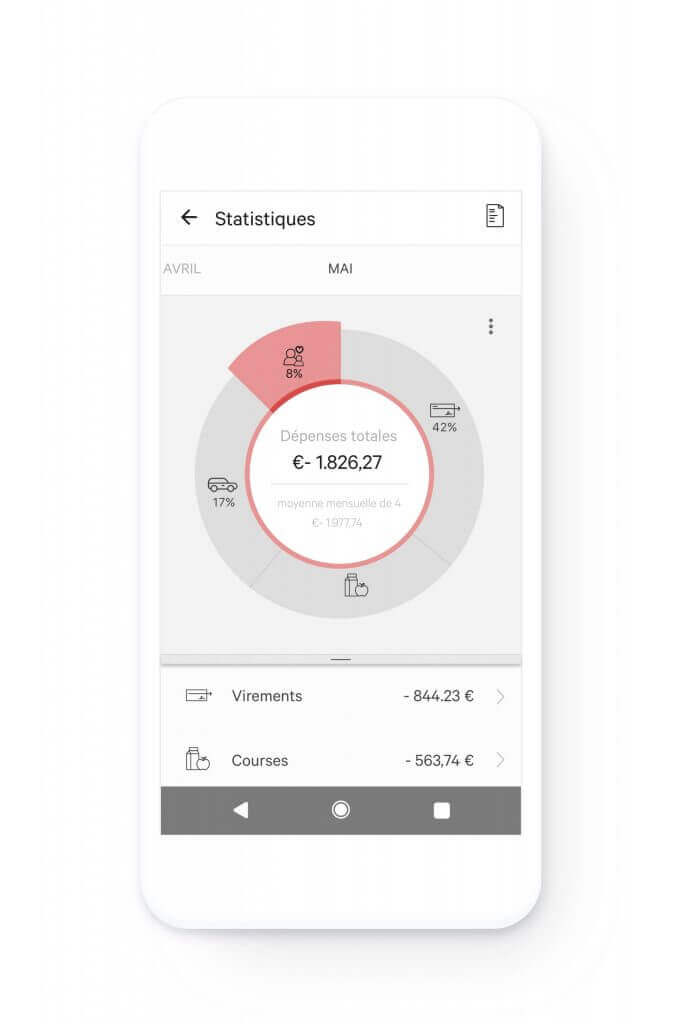

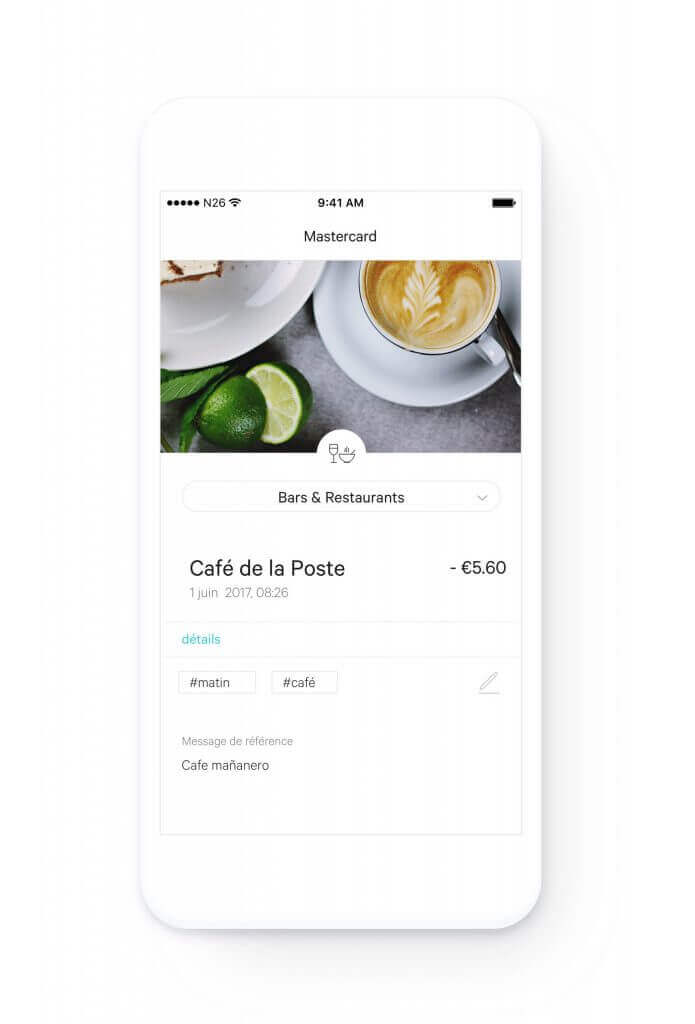

Another reason is the ease of use! When travelling it’s just super convenient to be able to access your account directly from your mobile phone and manage your budget centrally. Before leaving you make a deposit on the account and then you can see in real time where you are!

N26’s offer to reduce its foreign bank charges

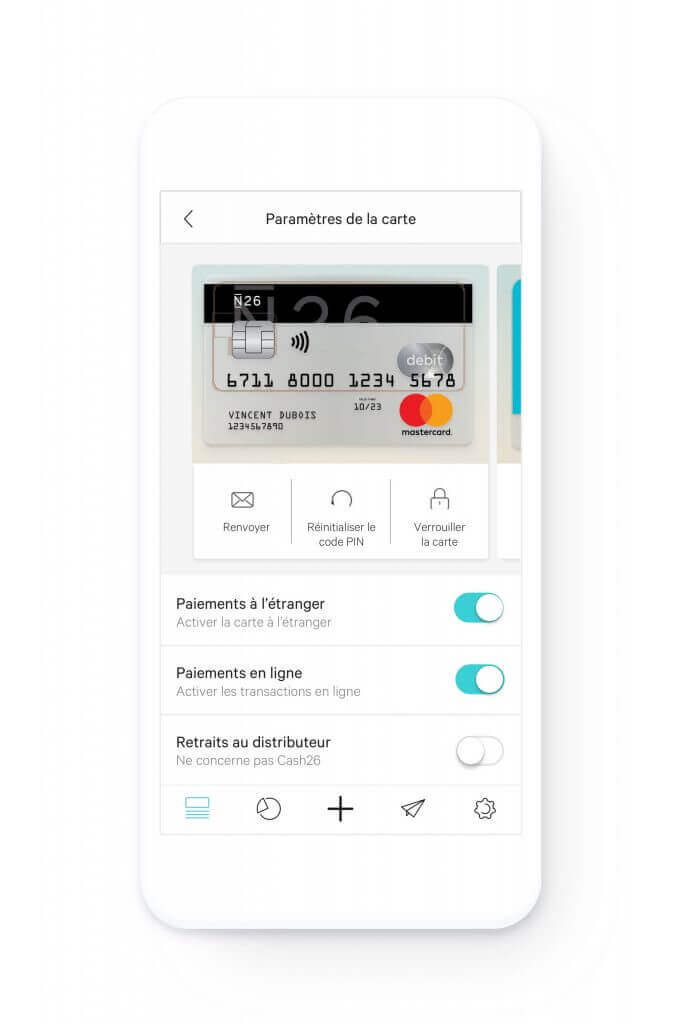

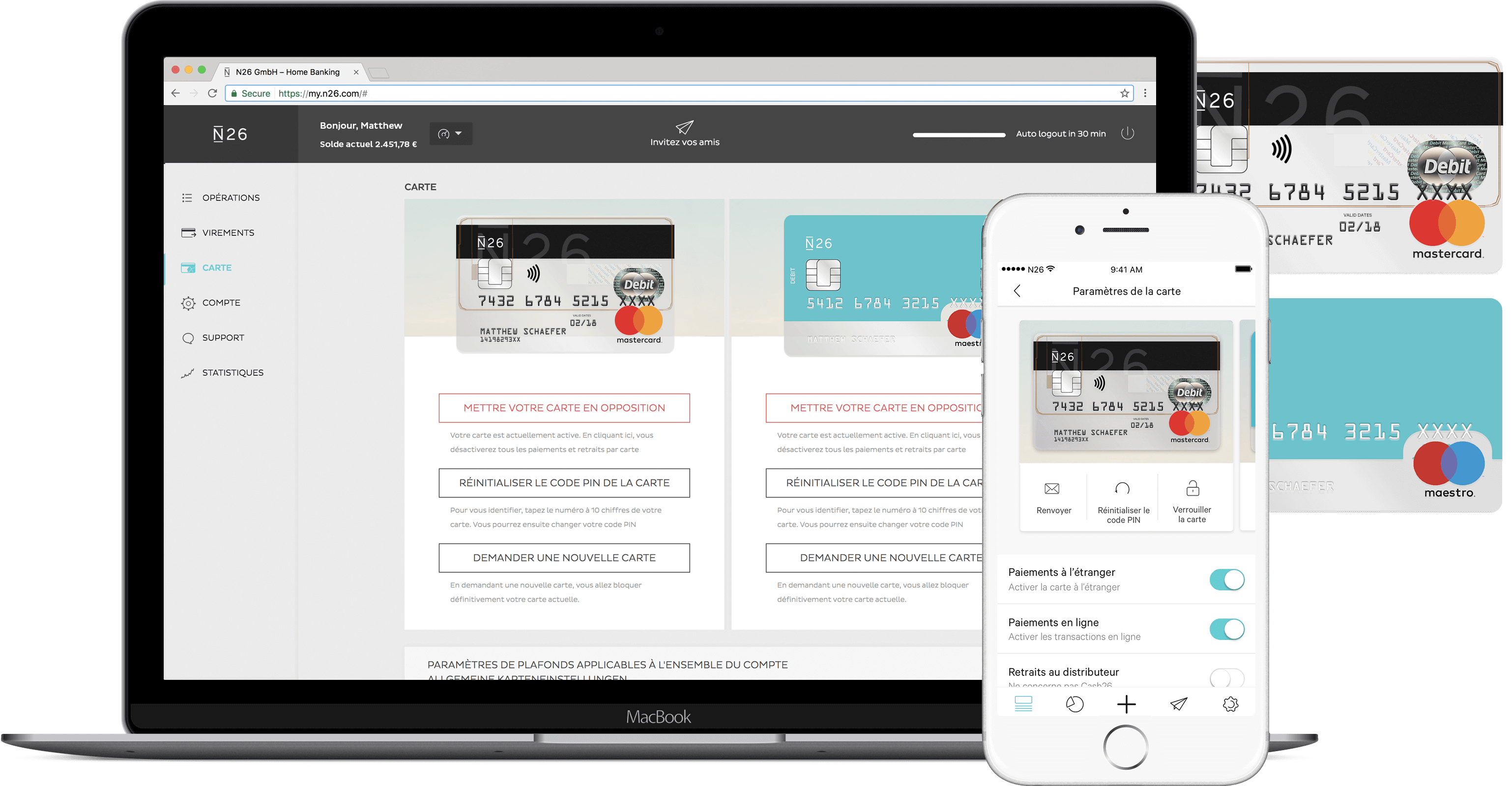

N26 offers 3 distinct services for individuals (actually 4, but the N26 metal offer isn’t very interesting, so we decided not to delve too deeply into it). One is free but comes with a few constraints, while the others are fee-based but offer a much wider range of services. Here’s a quick overview:

N26 Standard and N26 Smart: the account for occasional travellers

This account is absolutely free and entitles you to a Mastercard. (The card is also free of charge).

N26 Standard terms and conditions:

- No physical card, only a virtual card! You can order a physical card for €10.

- Rate: free

- 3 free € withdrawals per month. Then it’s €2 per withdrawal

- A commission of 1.7% is charged on withdrawals outside the euro zone.

- Free payment with no foreign exchange surcharge

- Free worldwide payment with virtual mastercard (unlike many banks, there are no exchange rate fees here).

- No telephone assistance available

N26 Smart terms and conditions :

- Fee: €4.9 per month

- You receive a physical card.

- 5 withdrawals per month in €, then €2 per withdrawal

- A commission of 1.7% is charged on withdrawals outside the euro zone

- Free payment with no foreign exchange surcharge

- create up to 10 sub-accounts to organize your budget

- Possibility of creating shared spaces between users to have a “common” account. This can be very useful when traveling

- you can choose the color of your card 😉

Who is this account for?

For the occasional traveller. If you make a few trips a year (in the euro zone or elsewhere) and on average you withdraw little money abroad. If you travel a lot and make a lot of withdrawals abroad, it is better to look at the N26 you.

Otherwise, the main difference between standard and smart is shared space and sub-accounts. If you’re a solo traveler (or you don’t need a shared account), and the option of organizing your budget seems superfluous, it may be more appropriate to take the free account and add 10€ to get a physical card (it’s cheaper than paying 4.9€ per month) 😉

N26 You: the account for people who travel a lot

The You version is N26’s premium and paid option. The price of this option is 9.90€ per month.

The conditions of use:

- 5 withdrawals in € per month for free. Then it’s 2€ per withdrawal

- Withdrawals outside the euro zone are 100% free

- Payment free of charge worldwide with the mastercard (unlike many banks there is no exchange rate commission)

- An Allianz travel insurance package (if you pay for the trip with your card): medical cover in the event of an emergency abroad, in the event of flight or baggage delays and insurance in the event of cancellation of your trip. .

- you can choose the color of your card 😉

The big difference between You and Smart is the free withdrawal fee! And on a round-the-world trip, this point pays for itself very quickly… To help you decide, as long as you plan to withdraw more than €300 per month from an ATM, the You option is already 100% amortized (with baggage, delay and bonus insurance).

How does it work? Create an online account

To open an account the procedure is extremely simple!

- Go to N26’s website and select the account you want

- Fill in the required fields.

- Confirm your email address by clicking on the link you received.

- Download the mobile application (iOS and Android) and connect.

- Proceed with identity verification (it is done by video-conference directly in the app)

- Once your identity has been verified your account is confirmed and you will receive your Mastercard as well as the Maestro by mail within 7 days.

- While waiting for your card to arrive you can already make a first transfer to your account and start using it as soon as you receive it!

What are the disadvantages of the neobank N26?

It’s all very nice… No or low withdrawal fees, easy access with your mobile phone from anywhere, fast and efficient customer service, does this mean this is the perfect bank?

So it’s perfect for travel! At the moment, N26 doesn’t offer the option of depositing cheques, but it has introduced the option of opening a savings account, and also the possibility of having a French, German IBAN (which simplifies tax declarations… you used to have to go through a special form to declare your accounts). Of course this will depend on your country of residency.

To be honest, there aren’t many drawbacks to using N26 as a travel complement. Master Card is accepted everywhere, the fees are very reasonable and the company has already been around for over 10 years and has a good reputation. All funds deposited are guaranteed up to €100,000 in the event of bank failure (as with a traditional bank).

Conclusion

We think it’s really a great solution for travelers in addition to your regular bank that will save you a lot of money on withdrawal fees abroad. If you’re Swiss and not with Postfinance (which is the only Swiss bank that doesn’t charge foreign withdrawal fees), you could have an N26 account as a complement to your bank to avoid getting ripped off, but after our comparison, we’d tend to believe that Neon is more advantageous for the Swiss (N26 You won’t be available to the Swiss in 2024) 😉 .

On the other hand, even if the N26 offer covers you with an Allianz insurance, the cover does not replace a travel insurance, in particular with regard to civil liability.

NB: This article contains partner links to N26. This means that if you go through our links to open an account we will receive a small commission (of course this does not change anything for you in terms of price). So if you want to support us in the work we do on our site do not hesitate to go through these links if you plan to open an account or to share this article with your friends. Thanks! 🙂